The Murrin Decision: How Long Should You Keep Tax Records?

If you’ve ever asked, “How long do I actually need to keep my tax records?”—you’re not alone.

A recent court case, Murrin v. Commissioner, is a great reminder that the answer isn’t always as simple as “three years.”

Let’s break it down in plain English.

What Was the Murrin Decision About?

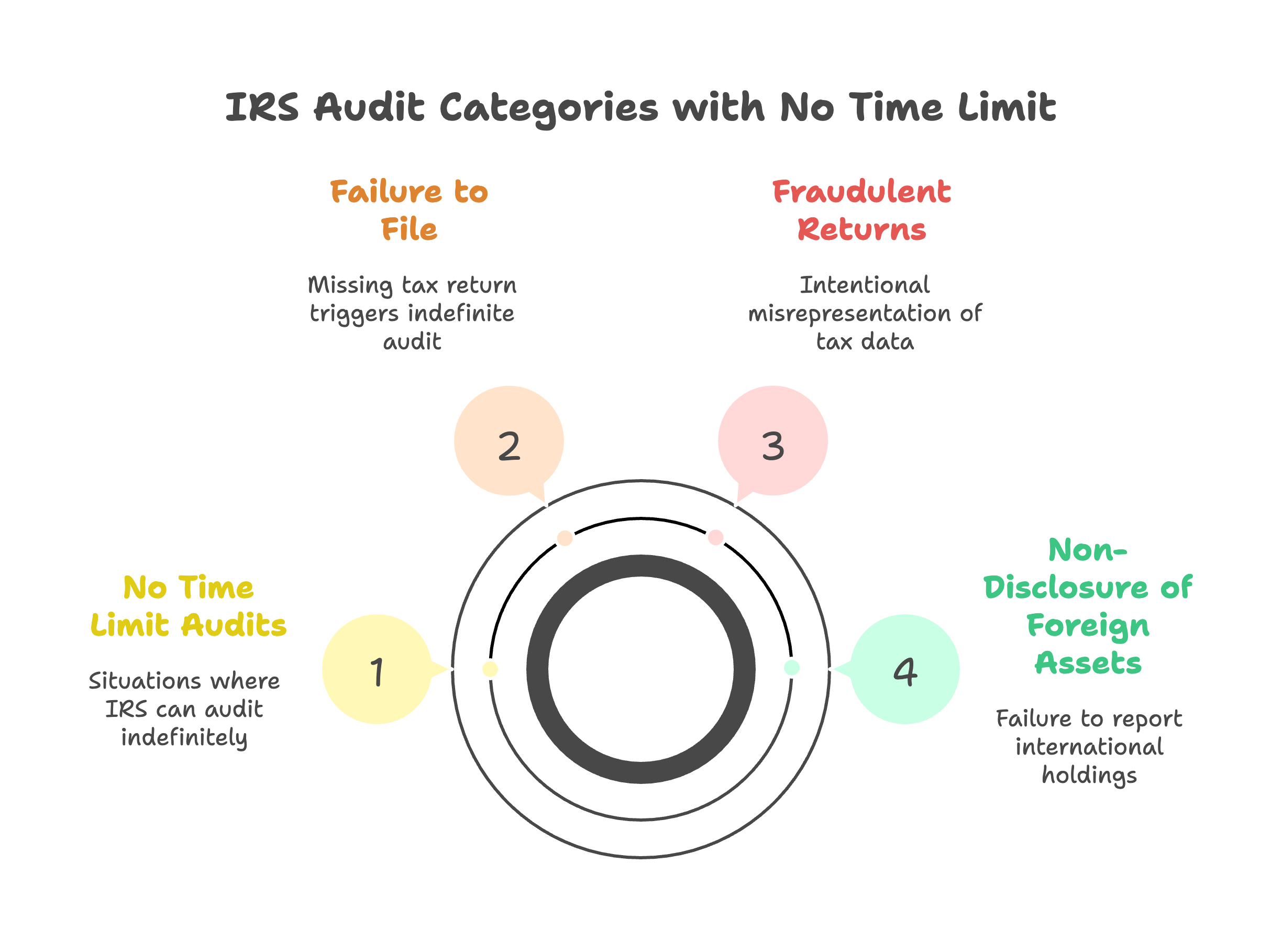

In the Murrin case, the taxpayer was audited and asked to support deductions from prior years—but didn’t have the records anymore. The IRS's unlimited audit window under Section 6501(c)(1) applies even when the taxpayer had absolutely no intent to evade taxes.

The result?

👉 The IRS disallowed the deductions.

👉 The taxpayer lost the case.

The key takeaway:

If you can’t prove it, you can’t deduct it—even if it was legitimate.

The “3-Year Rule” (and Why It’s Misleading)

You’ve probably heard:

“Keep tax records for 3 years.”

That comes from the general IRS statute of limitations—the time the IRS has to audit a return.

But here’s where it gets tricky:

The IRS can go back longer if:

You underreport income by more than 25% → 6 years

There’s fraud or no return filed → no limit

You claim certain losses or credits → longer review periods

You carry items forward (like depreciation or NOLs)

So in reality…

👉 3 years is the minimum—not the safe rule.

What You Should Keep (and For How Long)

Here’s a practical breakdown for your clients:

1. Tax Returns

Keep forever

They’re your financial “history file”

2. Supporting Documents (Receipts, Expenses, Bank Statements)

Minimum: 3 years

Safer: 6–7 years

This includes:

Expense receipts

Bank & credit card statements

1099s, W-2s, etc.

3. Assets & Depreciation Records

This is where most people mess up.

👉 Keep for the life of the asset + 3–7 years after disposal

Examples:

Equipment purchases

Vehicles

Real estate

Why?

Because the IRS can audit the gain/loss calculation years later, and that depends on your original records.

4. Business Ownership & Entity Documents

Keep forever

Includes:

Formation docs

Ownership records

Equity contributions

Real-World Example (Why This Matters)

Let’s say a client:

Bought equipment in 2018

Fully depreciated it

Sold it in 2025

If they tossed the 2018 records?

👉 They may not be able to prove basis

👉 That could mean paying tax on more gain than necessary

This is exactly the type of situation cases like Murrin highlight.

The Practical Rule I Recommend

👉 Keep everything for 7 years minimum

👉 Keep asset-related records much longer

👉 Store it digitally so it’s not a burden

Storage is cheap. Recreating records during an audit is not.

A Better Way to Store Receipts (Without the Paper Pile)

Keeping records doesn’t mean keeping stacks of paper.

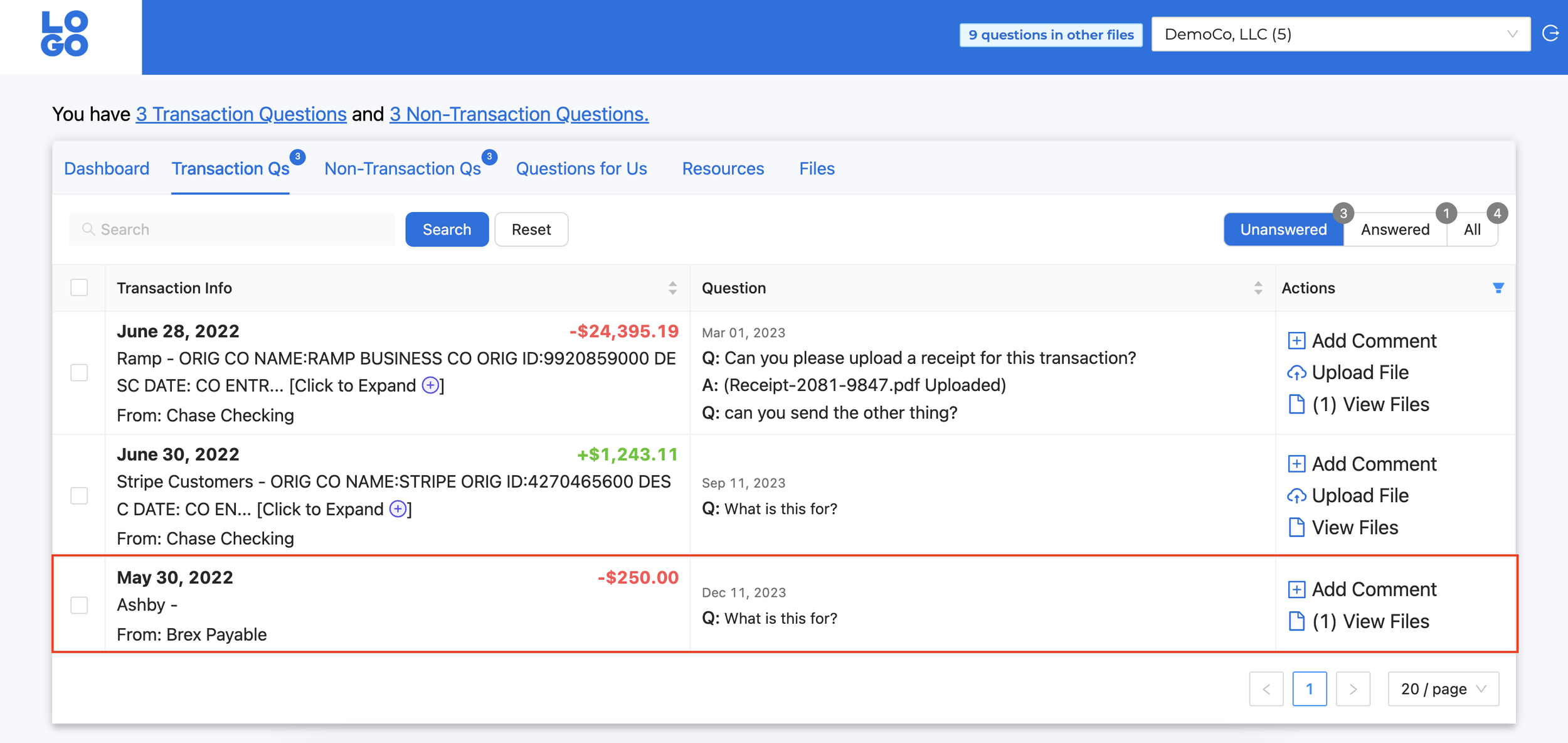

The easiest (and most reliable) way to stay organized is to store everything digitally—and attach documentation directly to the transaction.

Here’s how that works in practice:

👉 Upload receipts to a secure client portal

👉 Each receipt is reviewed and matched to the correct transaction

👉 The document is attached directly inside QuickBooks Online

So instead of digging through folders later…

Everything is already where it should be.

Why This Matters

If the IRS ever asks questions:

You don’t have to search your email

You don’t have to dig through paper files

You don’t have to guess what a charge was

👉 It’s all tied directly to the transaction in your books

What I Recommend to Clients

Keep it simple:

Upload receipts as you get them (or once per week)

Use a single system—not random folders

Let your bookkeeping system do the organizing for you

This turns recordkeeping from something you “catch up on”…

into something that’s handled automatically throughout the year.

The Real Benefit

This isn’t just about audits.

It’s about:

Cleaner books

Faster month-end close

Fewer questions and back-and-forth

And no scrambling at tax time

Final Takeaway

The Murrin decision reinforces a simple truth:

Good bookkeeping isn’t just about reports—it’s about documentation.

If records are missing, even valid deductions can disappear.

Want Help Staying Organized?

If your books (or your document storage) are a mess, that’s exactly what we fix.

Clean books. Clear records. No scrambling if the IRS ever asks questions.