QuickBooks Online Reconciliation Changes Coming Soon

Within the next few weeks, what has currently been available as only an option in QuickBooks Labs (Gear icon, under Your Company), the QuickBooks reconciliation will become live.

Reconcile - Opening Screen

The look and layout of all the screens will be totally different.

All transactions can be shown in list format on one page.

Any changes to transactions already reconciled will trigger a warning the next time an account is reconciled.

Discrepancy Warning

The Reconciliation Discrepancy report makes it easy to find out what has changed.

Reconciliation Discrepancy Report

I especially like the new Find filter option inside the reconciliation screen.

Find Transaction in Reconciliation

And the bigger warnings about reconciling when the difference isn't zero.

Reconciliation Warning about Non-Zero Difference

I am so familiar with the current reconcile mode that I have never warmed up to the newer way in QuickBooks Labs. But I think this will be a great improvement for users that may be new to QuickBooks Online or just have a hard time grasping the concept. I will certainly switch to it now so that I can be ready for my clients when they need help.

Part 2: How Do You Know If Your QuickBooks Financial Statements Are Correct?

If you track inventory in QuickBooks, you may already know how challenging it is to set up and maintain correct numbers. Typical for businesses that have over a million dollars worth of inventory or that need additional capital or lines of credit, a correct balance sheet is paramount.

Incorrect setup and erroneous data entry can lead to major problems with the numbers on a profit and loss and balance sheet report.

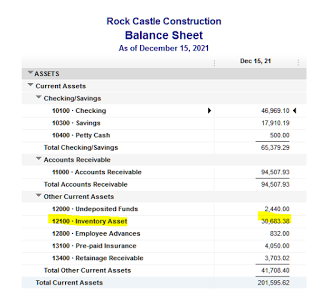

The total for the Inventory Asset account (the one that QuickBooks uses by default with inventory turned on) on the Balance Sheet (on accrual basis) and the Total Inventory at the bottom of the Asset Value column on the Inventory Valuation Summary reports should be equal.

If they don't match, here are some of the possible reasons why:

One or more inventory items were set up with an account other than inventory asset. This would skew the balance on the Balance Sheet. For example, to troubleshoot, go to the Item list | Right click and select Customize Columns and add the COGS Account, Account (Income), and Asset Account. Next, make sure that the accounts for each item is of the correct type. In this example, a COGS type account was used instead of the Inventory Asset account for the asset account.

An expense transaction was entered using the Expenses tab and the inventory asset account.

A journal entry was entered using the inventory asset account. Journals should never be used to change the value of this account; only inventory adjustments should be used to change the quantities and/or values of inventory items.

The two above are harder to troubleshoot to find the discrepancy. Drill down on the inventory asset amount on the balance sheet. Filter by transaction type and select: Check, Bill, Journal. Looking for the amount of the discrepancy also helps, unless there are many transactions that were entered incorrectly.

If you have the accountant version of QuickBooks or have a Certified QuickBooks ProAdvisor, it is much easier to find using the Reclassify Transactions tool. By selecting "Non-Item-Based" for Show transactions, only transactions that used the inventory asset account without using an item will be displayed.

How Do You Know If Your QuickBooks Financial Statements Are Correct?

Before sending your Profit & Loss and/or Balance Sheet reports from QuickBooks to your tax preparer or before you file your taxes yourself, you may want to continue reading.

There are several litmus tests to confirm that what is in your QuickBooks is correct and that your financial statements reflect this.

If you invoice (use Accounts Receivable) your customers out of QuickBooks, then you may want to make sure that the Total Income on your Profit & Loss report on an accrual basis matches your Sales by Customer Summary report.

Sales (Income) should be reflected with transactions only such as invoices, sales receipts, credit memos, and refund receipts (QuickBooks Online only), not using deposits to income or journal entries. To find out where the discrepancy lies, run a profit and loss report by customer or job and compare with the sales by customer summary report totals for each.

Fortunately, QuickBooks Online includes a Not Specified column to make this easier to find.

The culprit: 2 transactions, expenses, that were coded to income accounts.

This is another scenario in Quickbooks Desktop.

In comparing the reports, we find that the dollar amount discrepancy shows up for a Cost of Goods Sold account. Upon further drilling down, an invoice was used, but the item was not set up with an income account.

Once the item is fixed to either an income account or as two-sided (check box above Description checked), this fixes the reports and financial statements.

In my next post, I will show another test, so please subscribe below to get notifications to my blog. Thanks!